米PPI 6.5%が示す不都合なサイン: 消費者物価より先に仕入れ請求書を見る局面

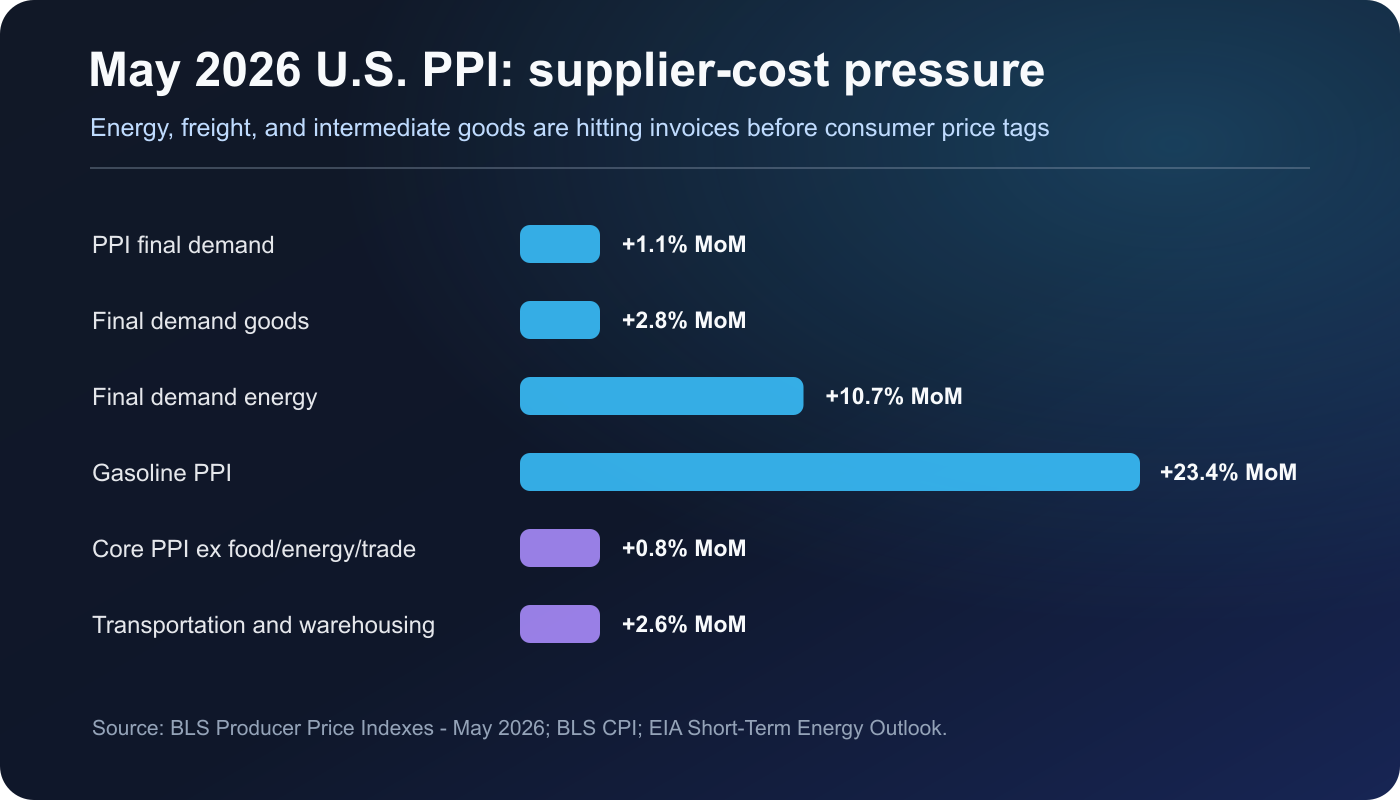

CPIは家計が見る価格表に近い。一方、PPIは企業が受け取る請求書に近い。2026年5月の米PPI最終需要は前月比1.1%、前年比6.5%上昇した。創業者や投資家にとって、これはマクロ指標である前にマージンの警告だ。

確認された事実

- BLS: final demand PPI rose 1.1% in May and 6.5% year over year.

- Final demand goods rose 2.8%; final demand energy rose 10.7%; gasoline PPI rose 23.4%.

- Core PPI excluding foods, energy, and trade services rose 0.8% in May and 5.1% year over year.

- CPI rose 0.5% month over month and 4.2% year over year; the energy index rose 23.5% over 12 months.

- EIA said Brent averaged $107/b in May and forecast around $105/b in June and July.

| 指標 | 変化 | シグナル |

|---|---|---|

| PPI final demand | +1.1% MoM | +6.5% YoY |

| Final demand goods | +2.8% MoM | largest since Dec. 2009 series start |

| Final demand energy | +10.7% MoM | 80% of goods advance |

| Gasoline PPI | +23.4% MoM | over half of goods advance |

| Core PPI ex food/energy/trade | +0.8% MoM | +5.1% YoY |

| Transportation and warehousing | +2.6% MoM | freight pass-through risk |

| Processed intermediate goods | +3.5% MoM | +13.3% YoY |

| Unprocessed intermediate goods | +4.9% MoM | +22.2% YoY |

なぜ重要か

PPIは機械的にCPIへ転嫁されるわけではない。固定契約やヘッジがある企業もあれば、顧客離れを恐れて値上げできない企業もある。だからこそ重要なのは、価格転嫁の前に粗利、割引、更新条件へ圧力が出る点だ。

The practical response is to review supplier invoices before the public price page is already under stress. Freight, fuel, payment fees, cloud credits, committed-use discounts, and AI inference usage should be separated so teams can decide where to absorb cost and where to explain price changes.

小規模チームのチェックリスト

• ベンダー費用をエネルギー、輸送、決済、クラウド、AI推論に分けて確認する。

• 値上げは利用量、配送速度、プレミアムSLA、海外決済など実際のコスト要因に結びつける。

• 利下げなし、エネルギー高、為替に5〜10%逆風という12カ月シナリオを置く。

リスクと反論

反論はボラティリティだ。エネルギー主導のPPI上昇は、石油フローが正常化すれば反転し得る。それでも運営計画を完全な反転だけに依存させるのは危うい。

Disclaimer

この記事は経済と市場を理解するための情報提供であり、金融助言や投資推奨ではありません。

出典

- BLS: Producer Price Indexes - May 2026

- BLS: Consumer Price Index Summary - May 2026

- EIA: Short-Term Energy Outlook, Global oil markets

- EIA: Short-Term Energy Outlook, U.S. petroleum product prices

- Federal Reserve: 2026 FOMC meeting calendar

- Federal Reserve: April 28-29, 2026 FOMC minutes

- Atlanta Fed: Market Probability Tracker methodology