美国PPI升至6.5%:真正的成本信号先出现在供应商账单里

Invest

浏览 55

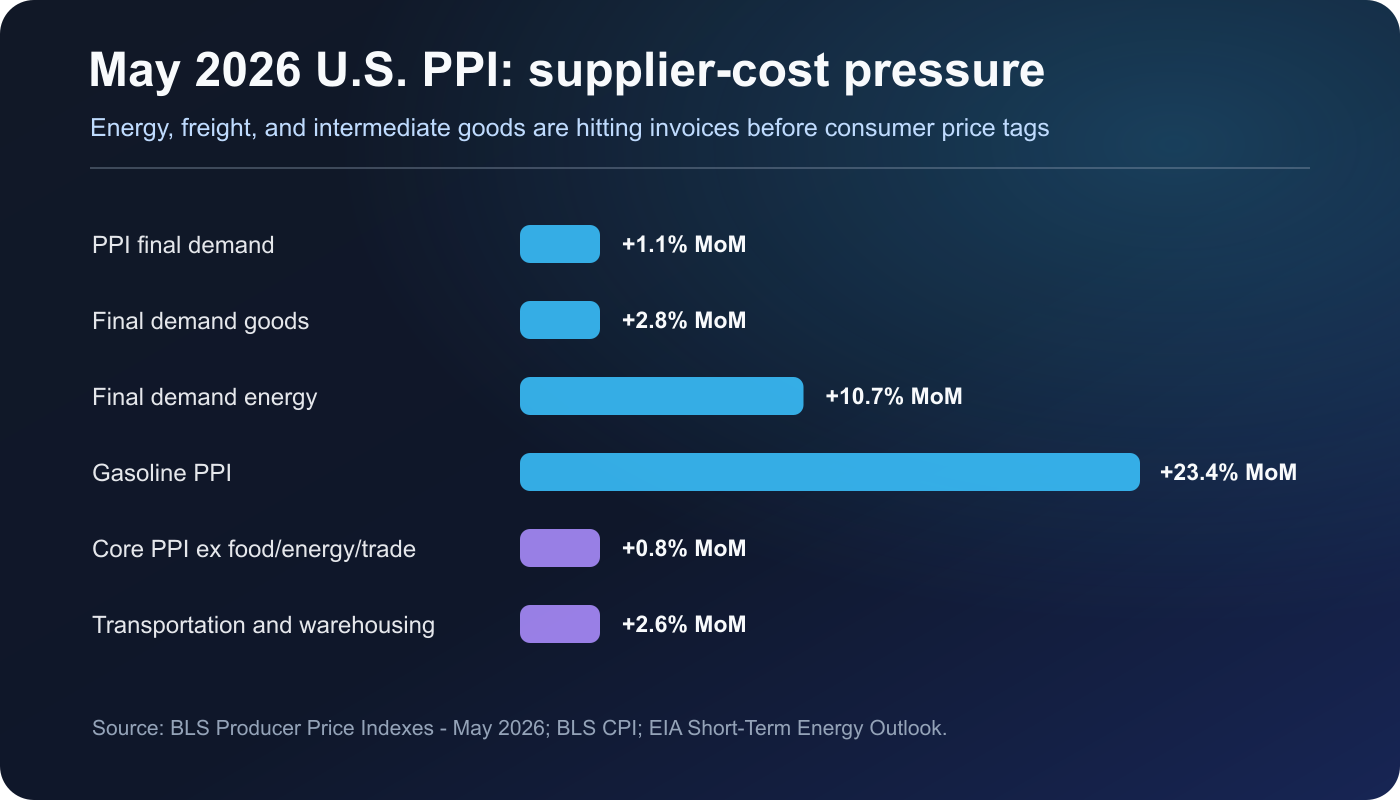

CPI更像消费者看到的价格标签,PPI更像企业提前收到的成本账单。2026年5月,美国最终需求PPI环比上涨1.1%,同比上涨6.5%。对创业者和投资者来说,重点不是宏观标题,而是利润率压力。

已确认事实

- BLS: final demand PPI rose 1.1% in May and 6.5% year over year.

- Final demand goods rose 2.8%; final demand energy rose 10.7%; gasoline PPI rose 23.4%.

- Core PPI excluding foods, energy, and trade services rose 0.8% in May and 5.1% year over year.

- CPI rose 0.5% month over month and 4.2% year over year; the energy index rose 23.5% over 12 months.

- EIA said Brent averaged $107/b in May and forecast around $105/b in June and July.

| 指标 | 变化 | 信号 |

|---|---|---|

| PPI final demand | +1.1% MoM | +6.5% YoY |

| Final demand goods | +2.8% MoM | largest since Dec. 2009 series start |

| Final demand energy | +10.7% MoM | 80% of goods advance |

| Gasoline PPI | +23.4% MoM | over half of goods advance |

| Core PPI ex food/energy/trade | +0.8% MoM | +5.1% YoY |

| Transportation and warehousing | +2.6% MoM | freight pass-through risk |

| Processed intermediate goods | +3.5% MoM | +13.3% YoY |

| Unprocessed intermediate goods | +4.9% MoM | +22.2% YoY |

为什么重要

PPI不会自动变成CPI。有些企业有固定合同或套保,有些企业无法在不损失客户的情况下涨价。因此信号的关键在于:成本先冲击毛利率、折扣和续约条款。

The practical response is to review supplier invoices before the public price page is already under stress. Freight, fuel, payment fees, cloud credits, committed-use discounts, and AI inference usage should be separated so teams can decide where to absorb cost and where to explain price changes.

小团队清单

• 在供应商复盘中拆分能源、运输、支付、云和AI推理成本。

• 把涨价绑定到真实成本驱动:用量、快速配送、高级支持或跨境支付。

• 加入12个月情景:不降息、能源成本更高、汇率逆风5%到10%。

风险与反方观点

反方观点是波动性。若石油流动恢复正常,能源驱动的PPI跳升可能回落。但经营计划不应只押注完美逆转。

Disclaimer

本文仅用于经济和市场背景说明,不构成金融建议,也不是任何资产的买卖建议。

来源

- BLS: Producer Price Indexes - May 2026

- BLS: Consumer Price Index Summary - May 2026

- EIA: Short-Term Energy Outlook, Global oil markets

- EIA: Short-Term Energy Outlook, U.S. petroleum product prices

- Federal Reserve: 2026 FOMC meeting calendar

- Federal Reserve: April 28-29, 2026 FOMC minutes

- Atlanta Fed: Market Probability Tracker methodology