Broadcom’s AI Chip Numbers Show the Next Cost Layer After GPUs

Most AI infrastructure conversations still start with NVIDIA GPUs. Broadcom’s Q2 fiscal 2026 results point to the next layer: once hyperscale customers have enough demand to optimize specific workloads, the bottleneck shifts from “can we get accelerators?” to “which custom chips, networking fabrics, and software economics produce the lowest repeatable cost?”

This is not a stock recommendation. It is a decision note for founders, solo builders, SaaS operators, and investors who need to understand how custom AI accelerators and AI networking may change product margins. The short version: AI unit economics are becoming a stack problem. Model choice matters, but so do routing, network cost, capacity commitments, cloud provider margins, and whether infrastructure vendors can turn AI demand into durable free cash flow.

Confirmed Facts

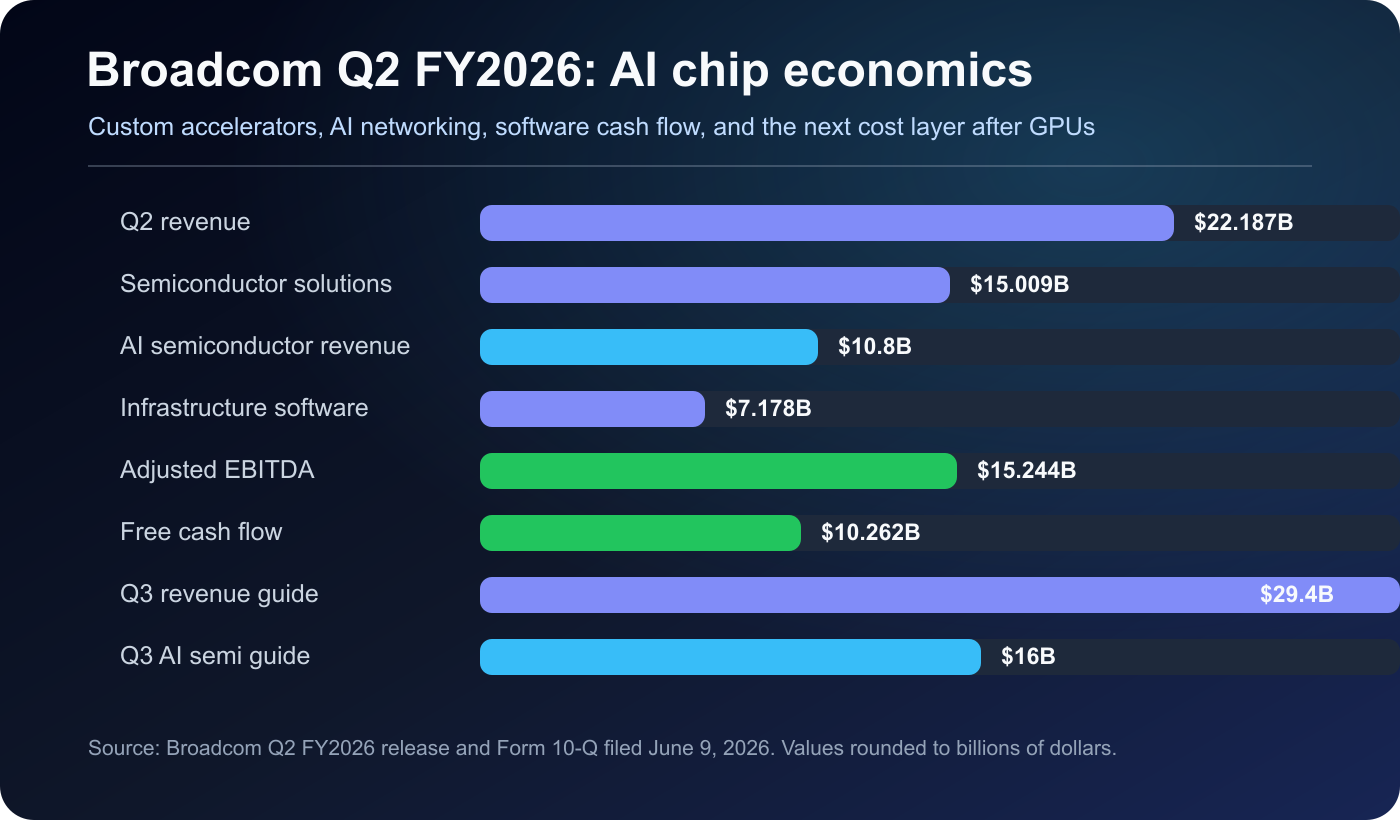

- Broadcom reported Q2 fiscal 2026 revenue of $22.187 billion for the quarter ended May 3, 2026, up 48% from the prior-year period.

- Adjusted EBITDA was $15.244 billion, or 69% of revenue. Operating cash flow of $10.493 billion less $231 million of capital expenditures produced $10.262 billion of free cash flow, or 46% of revenue.

- Semiconductor solutions revenue was $15.009 billion, up 79% year over year. Infrastructure software revenue was $7.178 billion, up 9% year over year.

- CEO Hock Tan said Q2 AI semiconductor revenue was $10.8 billion, up 143% year over year, and that Q3 AI semiconductor revenue is expected to reach $16.0 billion, up more than 200% year over year.

- Broadcom guided Q3 fiscal 2026 revenue to approximately $29.4 billion, up 84% from the prior-year period.

- The June 9 Form 10-Q showed $19.628 billion of cash and cash equivalents, $62.655 billion of long-term debt, and inventory rising to $4.328 billion from $2.270 billion at November 2025.

| Metric | Value | Context |

|---|---|---|

| Q2 revenue | $22.187B | +48% YoY |

| Semiconductor solutions | $15.009B | +79% YoY |

| AI semiconductor revenue | $10.8B | +143% YoY |

| Infrastructure software | $7.178B | +9% YoY |

| Adjusted EBITDA | $15.244B | 69% of revenue |

| Free cash flow | $10.262B | 46% of revenue |

| Q3 revenue guide | $29.4B | +84% YoY |

| Q3 AI semi guide | $16B | >200% YoY |

Interpretation: AI Infrastructure Is Not a GPU-Only Market

The important shift is that AI infrastructure is moving from a pure accelerator shortage story into a workload-specific cost optimization story. Large clouds and model companies will continue to buy general-purpose GPUs. But at sufficient scale, they also have an incentive to design or source custom accelerators and high-speed networking around their own inference, training, and data-movement patterns. Broadcom sits in that second lane.

For small teams, this does not mean designing chips. It means reading cloud economics more carefully. If hyperscalers lower the cost of certain workloads through custom silicon, the savings may flow through as cheaper API calls. Or they may stay inside premium tiers, dedicated capacity, low-latency regions, and enterprise contracts. Assuming that all AI API prices will fall evenly is therefore too simple.

The VMware and infrastructure software layer matters too. Broadcom’s quarter produced large free cash flow, but the 10-Q also shows substantial long-term debt and a sharp increase in inventory. AI semiconductor growth is most powerful when paired with software cash flow and disciplined working capital. If customer concentration, inventory, or debt concerns rise, the market will demand a much higher confidence level from the same headline growth numbers.

Market Narrative Signals

Post-earnings coverage framed the quarter as strong numbers meeting even stronger expectations. That distinction matters. Revenue, AI semiconductor revenue, and free cash flow were all large. Yet the market conversation quickly moved to Q3 AI guidance, hyperscaler dependence, and whether large customers such as Google, Meta, OpenAI, and Anthropic will keep relying on Broadcom-led custom silicon programs or diversify over time. Treat that narrative as a map of questions, not as standalone evidence.

Second-Order Effects

What to watch over the next 6 to 12 months

• Average AI API prices may fall while premium inference, low latency, and reserved capacity stay expensive.

• Cloud providers are likely to segment pricing more aggressively by GPU, ASIC, networking, region, and service-level guarantee.

• SaaS teams should price AI features by workload cost, not just by whether the feature “uses AI.”

• Investors should pair AI revenue growth with free-cash-flow conversion, inventory, customer dependence, and long-term debt.

Checklist for Builders, Small Teams, and Investors

- Product teams: split AI features into classification, retrieval, summarization, generation, and verification; track cost and latency for each step.

- Founders: launch “unlimited AI” only with usage caps, speed limits, premium-model upsells, and clear abuse controls.

- Developers: add caching, batching, smaller-model routing, and retry limits before sending every request to the most expensive model.

- Investors: put AI revenue growth, free cash flow, inventory growth, customer dependence, and long-term debt in the same table.

- Operators: cloud quotes should include networking egress, region premiums, reserved commitments, and dedicated-capacity costs, not just accelerator type.

Risks and Counterarguments

The main counterargument is concentration. Custom AI silicon can be more sensitive to a small number of hyperscale customers than a broad merchant-chip market. If customers design more of the stack themselves or diversify suppliers, a vendor’s growth rate can change quickly. Rising inventory also deserves attention because even a small demand miss can pressure both margins and working capital.

The opposite case is also real. AI networking and custom accelerators are hard to replace quickly, and infrastructure software cash flow can cushion part of the semiconductor cycle. The practical conclusion is not that every AI chip company is automatically attractive. It is that AI cost structure is moving from a single GPU variable into a combined equation of ASICs, networking, software cash flow, and customer concentration.

Disclaimer

This article is informational business and market commentary, not financial advice. It is not a recommendation to buy, sell, or hold any security. Make investment decisions independently based on your own financial situation and risk tolerance.