The U.S. Jobs Surprise: Why Cost Runway Matters More Than Rate-Cut Hopes

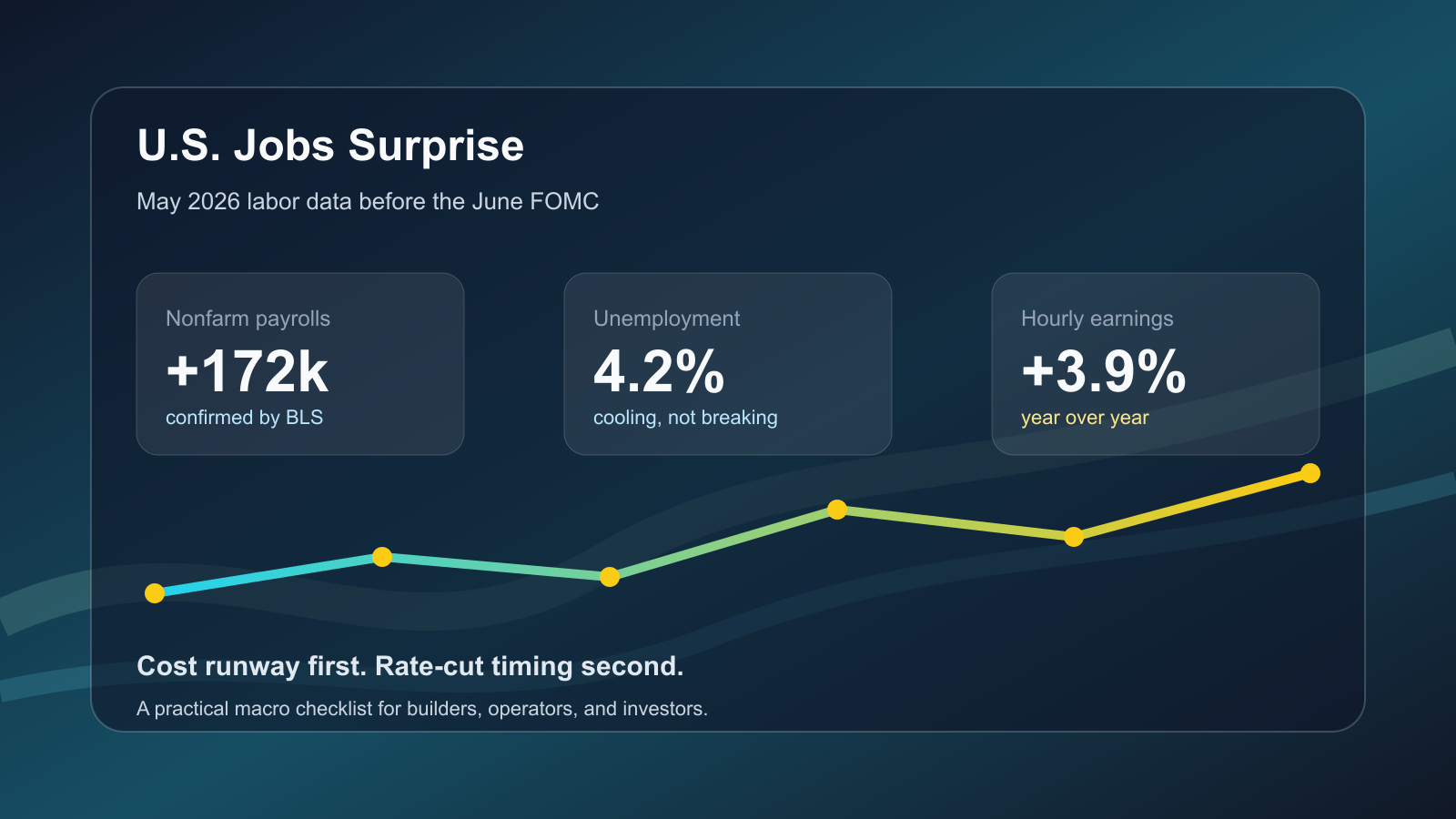

For teams waiting for rate cuts, inflation is not the only uncomfortable number. The U.S. Employment Situation report released on June 5, 2026 showed nonfarm payrolls rising by 172,000 in May, unemployment at 4.2%, and average hourly earnings up 3.9% from a year earlier. That is an awkward mix for markets that wanted a clean slowdown story. Hiring has cooled, but it has not broken. Wage growth is slower than the post-pandemic peak, but still firm enough to matter for service costs.

This is not a forecast of the next Fed move. The practical question is narrower: if higher funding costs and wage costs last longer than expected, what should founders, solo builders, investors, and operators check first?

| Indicator | Confirmed number | How to read it |

|---|---|---|

| May nonfarm payrolls | +172,000 | A firmer labor print can push rate-cut expectations further out. |

| Unemployment rate | 4.2% | The labor market looks more like gradual cooling than a layoff shock. |

| Average hourly earnings | +3.9% YoY, +0.3% MoM | Wage-sensitive service costs are not cooling quickly. |

| June FOMC | June 16-17, 2026 | Markets now have to reprice jobs, inflation, and wage data together. |

Confirmed Facts

- The BLS reported that U.S. nonfarm payroll employment increased by 172,000 in May 2026.

- The unemployment rate was 4.2%.

- Average hourly earnings rose 0.3% month over month and 3.9% year over year.

- The Federal Reserve kept the federal funds target range at 4.25% to 4.50% in its April 29, 2026 FOMC statement.

- The next scheduled FOMC meeting is June 16-17, 2026.

Interpretation: Why This Mix Is Hard

A weak jobs report would have made the rate-cut story easier. Soft inflation would do the same. This report points to something more complicated: the labor market is cooling, but not collapsing, and wage pressure is not disappearing quickly. The June Beige Book also described an economy where price pressure, labor-market adjustment, and demand softness coexist across districts. That is the environment many small teams actually feel: revenue does not accelerate like it used to, but payroll, financing, software, cloud, and service costs decline slowly.

The market narrative splits here. One camp sees the jobs surprise as support for a soft landing. Another argues that wage growth near the high-3% range gives the Fed less room to ease quickly. Axios captured the immediate narrative shift: the report weakened the case for pricing an imminent labor-market break. But that does not automatically make it cleanly bullish for every risk asset.

Second-Order Effects For Builders And Investors

First, SaaS and digital operators should watch burn rate before discount rates. If rate cuts move later, new funding rounds, refinancing plans, and paid acquisition payback periods all face a higher hurdle. Hiring ahead of a hoped-for easing cycle can become expensive if the cycle is delayed by one or two quarters.

Second, sticky wage pressure changes the ROI math for automation. Customer support, content operations, data cleanup, reporting, and internal admin are no longer just “AI productivity” candidates. They are cost-defense candidates. When labor costs cool slowly and capital remains expensive, small automations that prove savings quickly matter more than broad transformation decks.

Third, dollar exposure deserves a separate review. Teams earning in won but paying for cloud, ads, data tools, and SaaS in dollars are indirectly exposed to the U.S. rate path through FX and vendor pricing. Even teams without U.S. customers can see margin leakage through dollar-denominated tools.

- Hiring: split must-fill roles from roles that can wait one quarter.

- Runway: recalculate cash using a scenario where rate cuts arrive one quarter later.

- Pricing: test whether wage and tooling costs can be passed through to customers.

- Automation: pick one repetitive workflow and measure savings within two weeks.

- FX exposure: track monthly cloud, SaaS, and ad spend billed in dollars.

Risks And Counterarguments

One jobs report cannot determine the policy path. CPI, PCE, jobless claims, and consumer data could weaken enough to pull rate-cut expectations forward again. Stronger employment can also support household income and reduce the risk of an abrupt demand shock. The point is not “tight policy forever.” The point is that cost structures built on a fast-rate-cut assumption are fragile.

What To Watch Next

Before the June FOMC, watch inflation data, wage details, jobless claims, and the Fed’s language around the balance of risks. Investors should review position size and liquidity before making a directional bet. Operators should use a more conservative payback period for hiring, tooling, and marketing spend.

Disclaimer: This article is for informational economic commentary only. It is not financial advice, investment advice, or a recommendation to buy or sell any security. Decisions should reflect your own situation and risk tolerance.