NVIDIA’s Earnings Show AI Infrastructure Is Now a Pricing Problem

The lazy read on NVIDIA’s latest earnings is that GPUs are expensive and demand is still huge. The more useful read is sharper: AI infrastructure has become a pricing system. It now affects cloud margins, inference API pricing, data-center power contracts, startup runway and the capital allocation choices of the largest software companies.

This is not a stock call. It is a decision note for builders, founders, operators and investors who need to understand what the latest verified numbers imply for product economics. The short version: if your product uses AI heavily, model quality is only half the story. Token cost, inference utilization, reserved capacity, supplier concentration and user-level cost controls are now core product strategy.

Confirmed facts

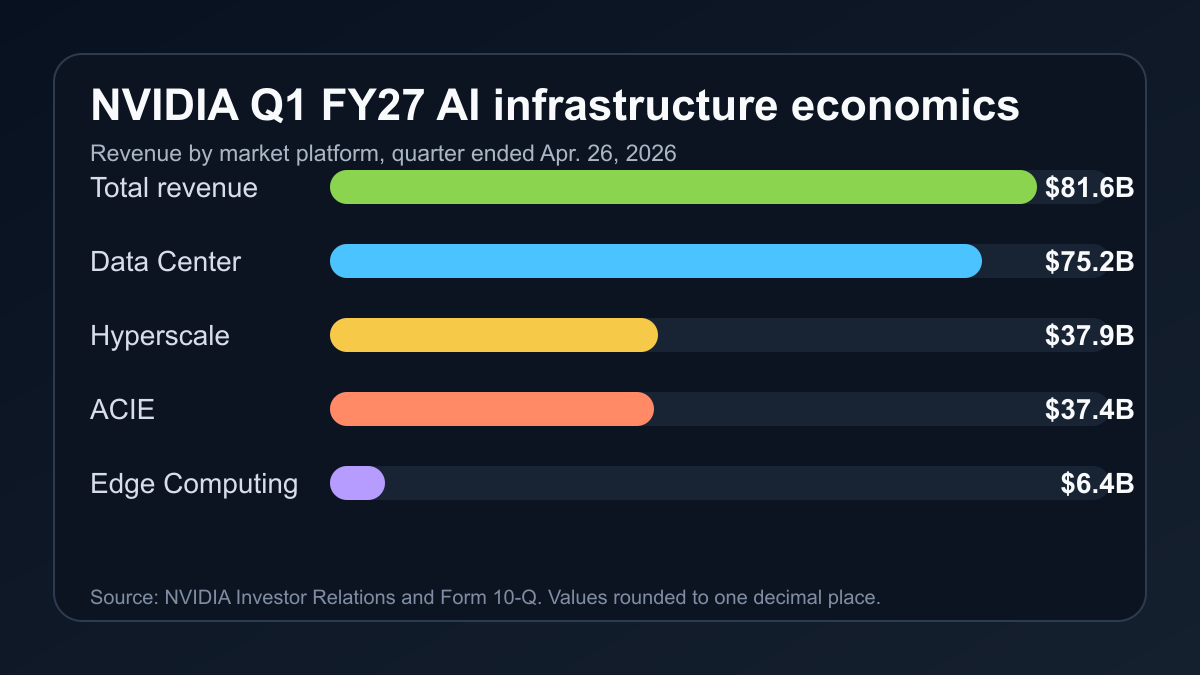

- NVIDIA reported Q1 fiscal 2027 revenue of $81.615 billion for the quarter ended April 26, 2026, up 85% year over year and 20% sequentially.

- Data Center revenue was $75.246 billion. NVIDIA’s press release described Data Center revenue as up 92% year over year.

- Starting with Q1 fiscal 2027, NVIDIA shifted to a new market-platform reporting framework: Data Center and Edge Computing. Inside Data Center, Hyperscale revenue was $37.869 billion and AI Clouds, Industrial & Enterprise, or ACIE, revenue was $37.377 billion.

- The Form 10-Q says three direct customers represented 21%, 17% and 16% of total revenue in the quarter, all primarily attributable to Compute & Networking.

- GAAP gross margin was 74.9%, operating cash flow was $50.344 billion, and NVIDIA repurchased $20.2 billion of common stock during the quarter. On May 18, 2026, the board approved an additional $80.0 billion share repurchase authorization.

- For Q2 fiscal 2027, NVIDIA guided to $91.0 billion of revenue, plus or minus 2%, and said it was not assuming any Data Center compute revenue from China in the outlook.

Interpretation: AI cost is now a finance problem

Software teams often frame AI adoption as a model-quality choice: use a stronger model, get a better product. NVIDIA’s new disclosure suggests the market has already moved past that simple frame. Hyperscale covers the public clouds and the largest consumer internet companies. ACIE covers AI clouds, industrial deployments, enterprise AI factories and sovereign or country-level infrastructure. The two pools are now nearly the same size.

For smaller teams, the most important number may not be revenue growth. It may be customer concentration. Three direct customers accounted for 54% of total revenue. That does not mean end demand is narrow, but it does mean much of the infrastructure supply chain still runs through a small set of purchasing and financing gates. Cloud providers commit capital first; the cost then flows down through reserved instances, inference API pricing, enterprise contracts, tighter free tiers and usage limits.

That changes how AI products should be built. “We added AI” is no longer enough. The durable question is whether the feature can preserve gross margin when usage repeats. A startup can win on model quality and still lose money if heavy users trigger expensive inference loops. A more disciplined team can use the same foundation models but survive longer by routing requests, caching repeated work, batching background jobs, using smaller models for low-risk tasks and pricing high-cost workflows honestly.

Market and community narrative

The market conversation was less about whether the headline numbers were strong and more about second-order questions: why the stock reaction was complicated despite the earnings beat, what a much larger dividend and buyback authorization signals, and how much growth can persist when China Data Center compute revenue is excluded from guidance. Those community threads are not factual sources; they are useful signals of what investors and builders are trying to resolve.

The deeper question is whether AI infrastructure remains an early growth market or is already behaving like a capital-goods cycle. If it is still early, high margins and strong demand can keep reinforcing each other. If it is a capital cycle, the next phase brings price competition, power bottlenecks, customer concentration, regulatory exposure and eventual utilization risk. The latest numbers do not prove either extreme. They show that AI demand is moving from experimental budgets into industrial-scale infrastructure commitments.

Second-order effects

What small teams and investors should track next

- Gross margin by AI feature, not just blended company margin.

- Inference sensitivity: input tokens, output tokens, image/video generation and agent loops should be modeled separately.

- Cloud contract structure: reserved capacity, credits, minimum commitments and termination terms matter more than list price.

- Supplier concentration: dependence on one model, one cloud or one GPU generation weakens pricing power.

- Power and data-center constraints: GPU supply can expand while real deployed capacity remains bottlenecked by electricity, cooling and networking.

First, AI API prices may not fall in a straight line. New hardware can reduce token cost, but if demand grows faster than effective capacity, premium inference capacity can stay expensive. Second, big-tech capital expenditure behaves like rent for the rest of the software ecosystem. If infrastructure costs stay high, SaaS vendors will push AI features into higher tiers, add usage caps or meter workflows more aggressively.

Third, investors need to look beyond revenue growth. Customer concentration, China exposure, working capital, inventory, share repurchases and ecosystem investments all matter. NVIDIA’s 10-Q shows non-marketable equity securities of $42.336 billion at quarter-end, with net additions of $17.899 billion during the quarter. That can be read as ecosystem-building strength. It can also raise a harder question: how much AI demand is being reinforced by capital flowing among the same infrastructure ecosystem participants?

Practical checklist

- Product teams: create a feature-level AI cost dashboard. Track average token cost per user, peak-hour cost and cache hit rate next to pricing decisions.

- Founders: be careful with “unlimited AI” promises. They are attractive in onboarding and dangerous when usage compounds.

- Developers: design model routing early. Classification, drafting, retrieval, reasoning and final verification do not need the same model every time.

- Investors: pair revenue growth with concentration, cash conversion, inventory, repurchase funding and regulatory exposure.

- Operators: do not price your own product solely on the hope that GPU costs will fall. If usage grows faster than unit-cost improvements, bills still rise.

Risks and counterarguments

The strongest counterargument is that supply expansion eventually lowers prices. NVIDIA’s Q2 guide and Data Center growth indicate strong demand, but rapid infrastructure buildouts can also create oversupply later. Model efficiency may reduce the GPU time required for the same task, and competing chips or custom ASICs can take specific workloads.

The second risk is demand quality. If customers are generating durable cash flow from AI services, the cycle is stronger. If they are buying infrastructure mainly because competitors are doing the same, the cycle becomes more fragile. That is why the latest earnings matter: the numbers are powerful, but the key question is how much of this demand is recurring economic demand rather than front-loaded strategic spending.

Disclaimer: This article is for informational purposes only and is not financial advice or a recommendation to buy, sell or hold any security. Make investment decisions independently based on your own financial situation and risk tolerance.